- View from the Arch

- Posts

- $CRCLE God Candle, Central Bank Woes & Scale AI Customers Scramble

$CRCLE God Candle, Central Bank Woes & Scale AI Customers Scramble

View From the Arch #89

Salutations to all the new readers!

This Week in Crypto

Honestly, it was another reasonably quite week in crypto - which makes my job in this section reasonably easy…

Farside Investors

As you can see it was a healthy week for the ETF complex, and treasury companies continued to gobble up the corn:

It was a great week for bald CEOs with circle (and Coinbase) absolutely ripping face:

Circle:USD

Honestly, it turns out all you needed to do was ape the Circle IPO and then sail off into the sunset. I think a relatively free trade would be to long Coinbase and short Circle over the next 6-12 months (categorically not financial advice).

The simple fact is: ~50 of Circle’s revenue is paid out to Coinbase. So Circle’s core business is effectively revenue-sharing its cash cow with the guy across the table.

Meanwhile, Coinbase runs a multi-pronged business with trading, custody, infra, and broader distribution. Circle… earns interest. That’s basically it.

Coinbase marketcap = $78B , Circle current marketcap = $52B. One has product-market fit in multiple verticals. The other is a high-beta interest-rate play with low float and a heavy reliance on its largest partner.

Circle is super low float - which explains the price action here. However, frankly, I can’t tell if the marginal bid here is dumb retail looking for “stablecoin exposure” (unclear which boomer is doing this), or institutions piling in (unclear who’s signing off on buys at this valuation in size).

Neither make that much sense to me… but maybe I’m missing something. Given I wasn’t a strong buyer at anything >$7B (7.5x ago!!)… I’m probably missing something.

Circle is undoubtedly riding the momentum from Washington with the Senate passing the GENIUS Act 68–30, marking the first major stablecoin legislation to clear a chamber of Congress; it now heads to the House, where debate over whether to combine it with the broader CLARITY Act could complicate its path.

And finally, a couple of other headlines relating to Stablecoin’s:

This Week in TradFi

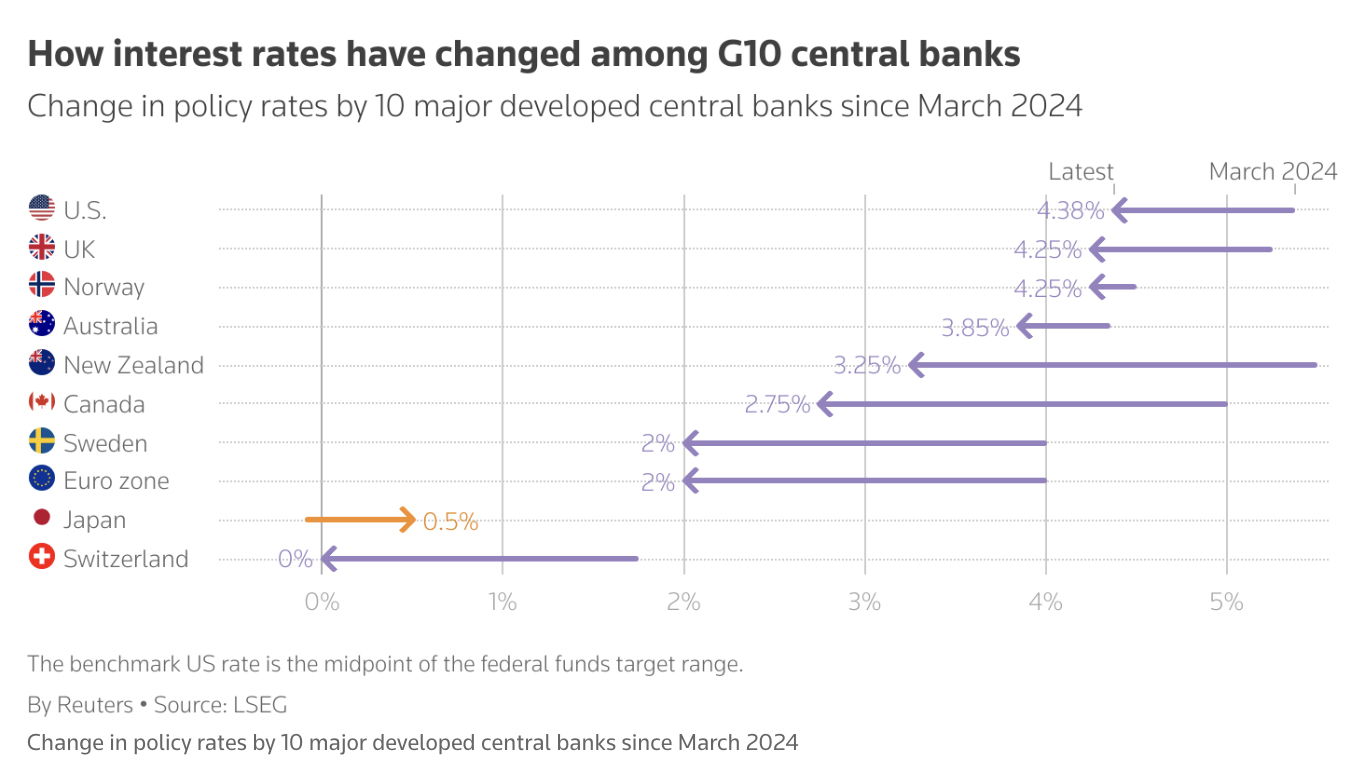

Conflict in the Middle East is increasing global uncertainty, putting central banks in an uncomfortable position as they try to figure out the best path forward.

Unsurprisingly the U.S. Fed kept the benchmark interest rate unchanged on Wednesday.

Investors had initially been counting on two quarter-point rate cuts this year, but the market is on edge after the Fed marked up its inflation outlook for the year.

The Fed revised inflation expectations to 3% this year, up slightly from its previous forecast of 2.7%.

And economic growth forecasts were revised downwards to 1.4%, vs. the March forecast of 1.7%.

The S&P ended nearly flat on Wednesday following Powell’s remarks.

The Bank of England also held interest rates steady at 4.25%, but said it was focused on a weaker labor market and higher energy prices as a result of the Middle East conflict.

London stocks dropped to an over two-week low yesterday as a result. The FTSE 100 closed down 0.6%.

Taiwan’s central bank also kept its policy rate unchanged yesterday and has indicated there are no plans for a rate cut at all this year.

Taiwan is a primarily export-driven economy and has been faring quite well with the continual increase in demand for AI applications.

And China is likely to keep its benchmark lending rate steady today, following monetary easing measures last month to help boost the economy.

Norway, on the other hand, surprised everyone and cut its policy interest rate by 25bps to 4.25% yesterday - its first borrowing costs reduction in five years.

In news other than just interest rates:

Oil prices are up and will likely continue to rise if tensions in the Middle East worsen.

Brent crude futures were up almost 2% on Thursday, and U.S. West Texas Intermediate crude was up 2.3%.

And the dollar was up yesterday - a reflection of investor preferences for perceived safe havens amidst Middle East tensions.

This Week in Tech

Last week we talked about Meta’s massive additional investment in Scale AI - and other AI companies are now acting on that investment.

Quick recap: Meta is investing almost $15B in the data-labeling company and taking a 49% stake in the startup. Additionally, CEO Alexandr Wang is going to help lead a new superintelligence lab at the company.

As a result, OpenAI is phasing out its work with Scale AI and cutting ties with the data provider.

A spokesperson told Bloomberg that the company had been seeking other data providers for more specialized data to continue to develop more advanced AI models.

Reuters also reported that Google is reconsidering its partnership as well. Google had planned to pay Scale AI $200M this year but is now reportedly having conversations with competitors and planning onto cut ties.

And OpenAI and Google aren’t the only ones - Turing CEO Jonathan Siddharth reported to TechCrunch that he’s already received interest from customers who “prefer to work with a partner that’s more neutral”.

Not exactly relevant but still funny:

Sam Altman says Meta is offering $100M signing bonuses to OpenAI staff.

Not $100M annual compensation, just the signing bonus!

He clowned Meta: “that’s not how you build a great culture.” Also said none of OpenAI’s best people are leaving.

This AI talent war is crazy.

— Yuchen Jin (@Yuchenj_UW)

11:23 PM • Jun 17, 2025

Antitrust laws may have another (potential) victim - Apple will be going to court for a class action lawsuit that alleges the company violates competition laws by forcing users of its devices to back up files and device settings on its own cloud storage service, iCloud.

The complaint also accuses Apple of not allowing third-party cloud services to access certain files, preventing them from offering full-service storage that could compete with iCloud.

Apple filed a motion to dismiss and cited security reasons as to why the company would not allow third-party cloud apps from accessing data like app data and device settings.

A California district court did not find those reasons to be sufficient, and denied Apple’s request to dismiss the case.

As usual, below are some fundraising announcements, M&A, and tech personnel changes that caught our eye:

AI-powered digital health startup Sword Health has raised $40M at a $4B valuation, led by General Catalyst.

Defense tech company Mach Industries has raised $100M at a $470M valuation, led by Khosla Ventures and Bedrock Capital.

Monetization platform Polar has raised a $10M seed round led by Accel.

Arch is building a next-gen wealth management platform for individuals holding Alternative Assets. Our flagship product is the crypto-backed loan, which allows you to securely and affordably borrow against your crypto.

Disclaimer: None of the above is financial advice, seriously.